Home | ARTS | Accounting For Managers

|

Introduction Of A New Product-Application Of Marginal Costing

Accounting For Managers - Management Accounting-Marginal Costing

Introduction Of A New Product-Application Of Marginal Costing

Posted On :

Sometimes, a product may be added to the existing lines of products with a view to utilise idle facilities, to capture a new market or for any other purpose.

1. Introduction

Of A New Product

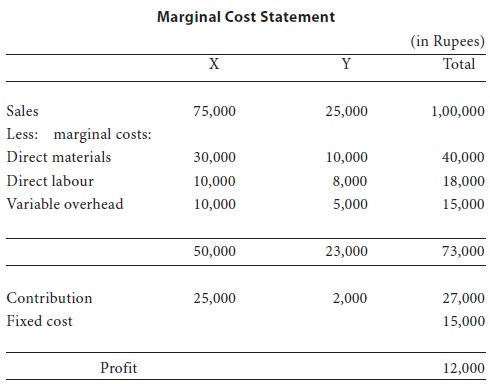

Sometimes, a product may be added to the existing lines of products with a view to utilise idle facilities, to capture a new market or for any other purpose. The profitability of this new product has to be found out initially. Usually, the new product will be manufactured if it is capable of contributing something toward fixed costs and profit after meeting its variable costs.

Illustration 5:

A concern manufacturing product x has provided the following information:

In order to increase its sales by rs.25,000, the concern wants to introduce the product y, and estimates the costs in connection therewith as under:

Fixed overhead Nil

Sometimes, a product may be added to the existing lines of products with a view to utilise idle facilities, to capture a new market or for any other purpose. The profitability of this new product has to be found out initially. Usually, the new product will be manufactured if it is capable of contributing something toward fixed costs and profit after meeting its variable costs.

Illustration 5:

A concern manufacturing product x has provided the following information:

Rs. | |

Sales | 75,000 |

Direct

materials | 30,000 |

Direct

labour | 10,000 |

Variable

overhead | 10,000 |

Fixed

overhead | 15,000 |

In order to increase its sales by rs.25,000, the concern wants to introduce the product y, and estimates the costs in connection therewith as under:

Direct

materials | 10,000 |

Direct

labour | 8,000 |

Variable

overhead | 5,000 |

Advise whether the product Y will be profitable or

not.

Solution:

Commentary: if product Y is introduced, the profitability of product X is not affected in any manner. On the other hand, product Y provides a contribution of Rs.2,000 Towards fixed cost and profit. Therefore, Y should be introduced.

Solution:

Commentary: if product Y is introduced, the profitability of product X is not affected in any manner. On the other hand, product Y provides a contribution of Rs.2,000 Towards fixed cost and profit. Therefore, Y should be introduced.

Tags : Accounting For Managers - Management Accounting-Marginal Costing

Last 30 days 961 views