Accounting For Managers - Management Accounting-Marginal Costing

Key Factor-Application Of Marginal Costing

Posted On :

A concern would produce and sell only those products which offer maximum profit.

Key

Factor

A concern would produce and sell only those products which offer maximum profit. This is based on the assumption that it is possible to produce any quantity without any difficulty and sell likewise. However, in actual practice, this seems to be unrealistic as several constraints come in the way of manufacturing as well as selling. Such constraints that come in the way of management’s efforts to produce and sell in unlimited quantities are called `key factors’ or `limiting factors’. The limiting factors may be materials, labour, plant capacity, or demand. Management must ascertain the extent of the influence of the key factor for ensuring maximisation of profit. Normally, when contribution and key factors are known, the relative profitability of different products or processes can be measured with the help of the following formula:

Contribution

Profitability = -----------------------

Key Factor

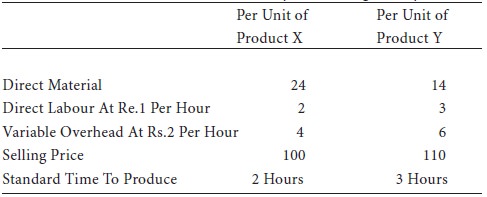

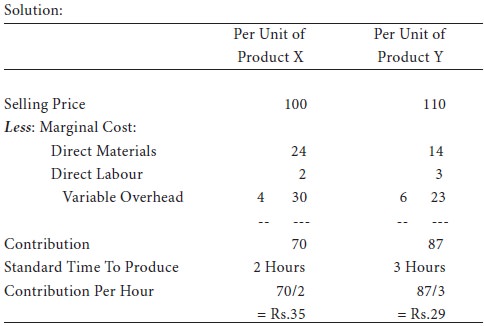

Illustration 7: from the following data, which product would you recommend to be manufactured in a factory, time, being the key factor?

Contribution per hour of product x is more than that of product y by rs.6. Therefore, product x is more profitable and is recommended to be manufactured.

A concern would produce and sell only those products which offer maximum profit. This is based on the assumption that it is possible to produce any quantity without any difficulty and sell likewise. However, in actual practice, this seems to be unrealistic as several constraints come in the way of manufacturing as well as selling. Such constraints that come in the way of management’s efforts to produce and sell in unlimited quantities are called `key factors’ or `limiting factors’. The limiting factors may be materials, labour, plant capacity, or demand. Management must ascertain the extent of the influence of the key factor for ensuring maximisation of profit. Normally, when contribution and key factors are known, the relative profitability of different products or processes can be measured with the help of the following formula:

Contribution

Profitability = -----------------------

Key Factor

Illustration 7: from the following data, which product would you recommend to be manufactured in a factory, time, being the key factor?

Contribution per hour of product x is more than that of product y by rs.6. Therefore, product x is more profitable and is recommended to be manufactured.

Tags : Accounting For Managers - Management Accounting-Marginal Costing

Last 30 days 4156 views