Strategic Management - Strategy Implementation

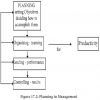

Types of Plans - Planning And Resources Allocation

The failure of managers to recognize that there are several types of plans has often caused difficulty in making planning effective.

The failure of managers to recognize that there are several types of plans has often caused difficulty in making planning effective. Plans encompass any cause of future action and hence vary as under.

Purposes or missions

Identifies the basic task of a firm or agency. Ex. Purpose of business is the production and distribution of goods and services

Dupont | - | Better

things through chemistry |

Kleenex | - | Production

and sale of |

paper

& products | ||

Hallmark | - | Social

expression of business |

J &

J | - | First

responsibility to doctors, |

nurses,

patients and mothers | ||

Dow

chemical | - | Sharing

world’s obligation for |

the

protection of the environment |

Conglomerates express their mission as ‘synergy’ which is achieved through combination of a variety of companies.

Therefore mission is the organization’s purpose and fundamental reason for existence. A mission statement is the broad declaration of the basic. Unique purpose and scope of operations distinguish the organization from others.

Objectives and goals

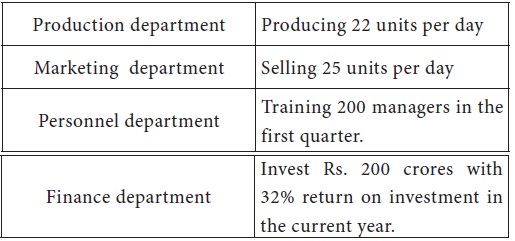

Planning aims at goal setting. Goals and objectives are ends towards the activity aimed. They represent the end toward organizing, staffing, leading and controlling. Each department may have its own goals, which contribute to objectives of organizations as illustrated below.

Goals

serve many purposes like the following |

| |||||||

*

Increase performance | *

Clarify expectations |

| ||||||

*

Facilitate the controlling function | *

Increased motivation |

| ||||||

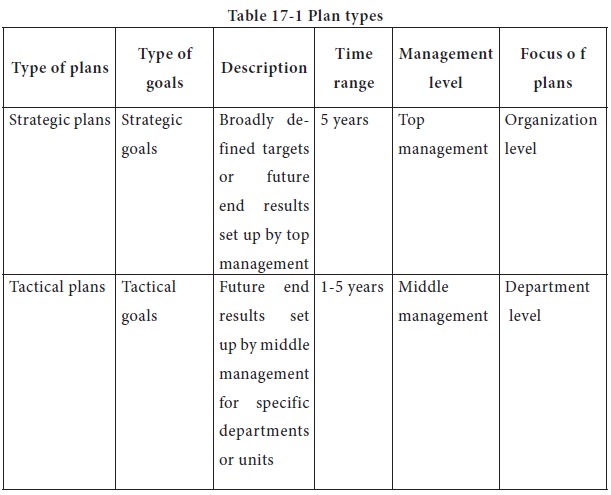

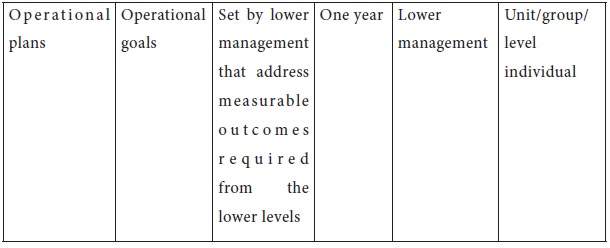

Goals

have levels that compare with hierarchy of organization as depicted in Table 17 - 1. | ||||||||

| ||||||||

Peter F.

Drucker gives eight

major areas for

goal setting by organizations. | |||||||

*Market

standing | *Innovation | ||||||

*Human

resources | *Financial

resources | ||||||

*Physical

resources | *Productivity | ||||||

*Social

responsibility | *Profit

requirements | ||||||

Strategies | |||||||

Strategies are grand plans in the light of what it was believed an adversary might or might not do. Strategy may be defined as follows. “Strategy is the determination of basic long term objectives of an enterprise and the adoption of courses of action and allocation of resources necessary to achieve these goals”.

A strategy might include such as marketing directly rather than through distributors or concentrating on proprietary products of having a full time of autos ex: General Motors.

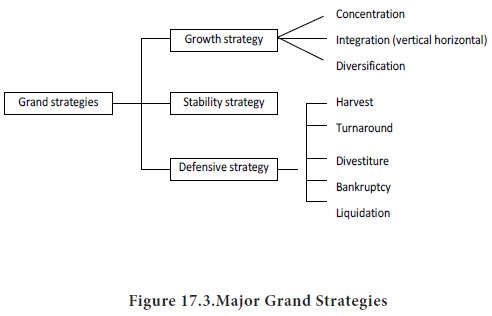

Strategies are of two types

Generic strategies - involve organization expansion in some select areas. The generic strategies include –

1. Overall cost leadership

2. Differentiation

3. Focus

Grand strategies - A master strategy that provides direction at the corporate level

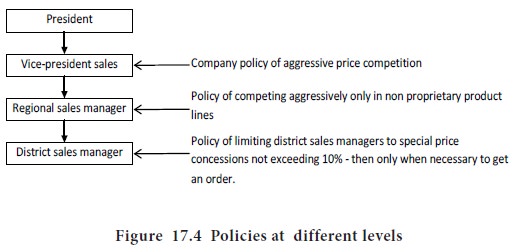

Policies

Policies are plans or general statements or understandings that guide or channel thinking in decision making. Policies define an area in which decision is to be made and ensure consistency to objectives. Policies help managers maintain control and delegate authority.

Policies exist at all levels in an organization. They may be major or minor. Policies include hiring trained engineers, encouraging employee suggestions, confirming to high standards, setting competitive prices, cost plus pricing etc. Companies can have policy manuals which may stipulate non-acceptance of gifts from suppliers, favours of entertainment or seek outside employment.

Making policies is difficult for

1. They are seldom defined in writing

2. Delegation of authority will create confusion

3. Actual policy may be difficult to ascertain and intended policy may not be clear.

Policies are necessary at different hierarchical levels as shown in Figure 17-4

Procedures

Procedures are plans that establish a required method of handling future activities. They are guides to action, rather than thinking and they detail the exact manner in which certain activities must be accomplished. Procedure is thus a prescribed series of steps to be taken under certain recurring circumstances. Well-established ones are called ‘Standard Operating Procedures’. Ex: In Banks SOPs govern how tellers handle deposits.

The following procedures are common and are across different departments.

Production

Department | - | release

of stock |

Traffic

Department | - | shipping

means & route |

Finance

Department | - | customer

credit approval, |

acknowledgement

receipts | ||

Marketing

Department | - | for

original order |

Rules

“A statement that spells out specific actions to be taken or not taken in a given situation”

Unlike procedures, rules do not normally specify a series of steps. They dictate what must or must not be done.

Ex: 1. “No Smoking” is a rule unrelated to procedure.

Policies guide decision making, but rules allow no discretion in decision making.

Programmes

Programmes involve different departments or units of organization composed of several different projects which may take about one year to complete. Programme may be defined as follows.

“A programme is a comprehensive plan that coordinates a complex set of activities related to a major non recurring goal”.

“Programmes are a complex of goals, policies procedures, rules, task assignments, steps to be taken, resources to be employed and other elements necessary to carry out a given course of action supported by budgets”.

Examples of programmes are

1. A major airline acquiring $400 million fleet of jets

2. Five year programme to improve status and quality of supervisors.

i. Dividing the project into parts

ii. Determining relationships and pulling in a sequence

iii. Deciding responsibilities for mangers

iv. Determining how to complete and what resources are necessary

v. Estimating time requirements

vi. Developing a schedule of implementation

A primary programme may trigger off a series of small programmes.

Budgets

Budget is a numberized programme. It can be defined as follows.

“Budget is a statement of expected results expressed in numerical terms”

Budget can be expressed in financial terms, labour hours, units, machine hours etc. It may show expenses, capital outlays, cash flows etc.

A budget is a fundamental planning instrument. Budget forces precision in planning.

• | Flexible/variable

budgets | - | vary

according to the level of | ||

output | |||||

• | Programme

budgets | - | an

agency to identify goals, | ||

develop

programmes to meet them and give cost estimates. | |||||

• | Operating

budget | - | A finance | plan for | each |

responsibility

during budget period. | |||||

• | Capital

budget | - | Budget for | Mergers | & |

Acquisitions,

divestiture of fixed assets. | |||||