Operations Management - Transportation / Assignment & Inventory Management

Terms associated with Inventory Management

Posted On :

In this section, let us gain some idea about various costs and terminology associated with Inventory Management.

Terms

associated with Inventory Management

In this section, let us gain some idea about various costs and terminology associated with Inventory Management.

For example, consider a production unit, which is manufacturing Instant Food mixes, using the same grinding and packing facilities for both ‘Idli-mix’ and ‘Kesari Mix’. Before they change the production run it is necessary to clean the grinder with left outs of previous runs. Some time, they may use some common materials to clear or using cotton waste to clearing the residues or some special chemicals to clean it. It may consume material and/or men or there is some amount of cost associated with the operations.

On the other hand, if we have to place an order as in the case of a Stockist/Dealer, the cost may range from simple clerical plus stationers plus postage to complex estimates such as placing a quotation. Here again it consumes labor and/or material, and finally can be bringing down to a cost element associated with it.

Thus, this is the cost incurred with the placement of an order or with the initial preparation of production facility such as resetting the equipment for production. The set up cost is usually independent of the quantity ordered or size of the production run.

It is the actual price; an item is produced or purchased (sold). In case of production it is the cost of producing an item and it may be a constant or variable one.

This represents the cost of carrying inventory in storage. It includes the interest on invested capital, storage space cost, insurance and handling cost. Holding costs are usually assumed to vary directly with the level of inventory as well as the length of the time the item is held in stock.

Holding cost consists of so many components with it and the type of storage such as own warehouses to rental warehouses, makes things much more complicated than expected. Above all, the accounting practices of many organizations may not support or sound enough to decide the cost estimates. Even though, the company owns the storage space, electricity expenses are met, the policies may not be very clear to arrive at the opportunity cost forgone by owning these facilities.

These are the penalty cost incurred as a result of running out of stock, when the commodity is needed. It generally includes the costs, due to loss of production, cost of idle equipment, the loss of goodwill of customers and the penalty of missing the delivery schedule.

In a study on FMCG segments, the stock out percentages of 85 prime brands, were estimated roughly around 25%, which means, out of these 85 fast moving brands, on an average, nearly 20 brands will be out of stock 4. These 85 brands, was in a position to control roughly 20% market share of the FMCG segment. The amount of revenue loss and loss of good will and ultimately loss of the customer base are going to be the consequences of shortages.

Recent survey reports of NCEAR say that brand switching is a common phenomenon in most of the FMCG product lines. Above all, the companies are trying for the same market share through the variety of consumer promotion tools. During the year 2001, almost 25-30 consumer promotions were offered in a month against the average of 5-6 5. In the case of rural consumers, the rate of brand switching is much higher than the urban chaps 6.

Some of the companies while purchasing make it compulsory to include a class on treatment on missing the scheduled delivery. Most of the times, very huge penalty such as the loss estimated as the case of missed scheduled will be entirely borne by the supplier and the missed scheduled used to estimate the performance of the vendor/seller/suppliers.

Demand is the number of units required per period and may be known exactly or known in terms of probabilities.

Problems

in which demand is known and fixed are called deterministic problems.

Problems in which demand is assumed to be a random variable are called stochastic problems. The demand is invariably probabilistic in nature for many real time situations. For some of the products, the demand may be seasonal also, such as soft drinks, cement etc.

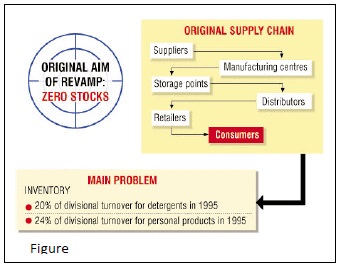

When an order is placed it may be of instantaneous delivery or it may require some time before delivery is effected. The time between the placement of order and its receipt is called lead-time. Again the lead-time may also follow probability distribution. I.e., the lead-time is certain or uncertain. Consider the example of a FMCG Distribution channel, which faced lot of problems with high amount of inventory and distribution efficiency.

If the distributor is placing order on, say

February 1, the order may be processed at the Storage point by 4or 5 the month,

he will get the stocks by end of 8 or 9. This will hold well if everything goes

as expected. If there is stock out of one or two of the products, then the lead-time

may vary further. If we refer the picture, the company has suffered with high

amount of inventory, which is almost 50% of the annual sales of the company.

The problem is estimating the demand and lead-time with certain amount of

accuracy.

Getting stocks again is called replenishment. Instantaneous replenishment occurs when the stock is purchased from outside. Uniform replenishment may occur when the procured from local manufacturer.

For example, an automobile manufacturer purchasing Tyres from the local Original Equipment Manufacturer, used to get stocks at some fixed intervals say everyday one truckload or 1000 Tyres instead of getting the entire estimated demand of 30,000 Tyres in a month at once. Some of the parts such as screws and bolts etc can be purchased at bulk and stored. Here the entire demand for the month is supplied at once.

Inventory control problem in which demand is assumed to be fixed and completely known is called Economic Order Quantity (EOQ) problems. If it is the context of production, the batch size to be produced is fixed and completely determined in advance, and then it is known as Economic Lot Size problems.

Generally demand is uncertain and cannot be pre determined completely. Lead-time is not always known exactly. The revenue forgone by not keeping adequate inventory i.e., cost of under stocking and sometimes payment of penalty for not meeting the delivery schedule are consequences of inadequate inventory levels. To overcome the situations of uncertainty in demand and lead-time, some extra stock is advisable so that shortages may not occur. This extra stock is known as buffer stock.

In this section, let us gain some idea about various costs and terminology associated with Inventory Management.

1. Set up Cost ( or) Ordering cost:(Cs)

For example, consider a production unit, which is manufacturing Instant Food mixes, using the same grinding and packing facilities for both ‘Idli-mix’ and ‘Kesari Mix’. Before they change the production run it is necessary to clean the grinder with left outs of previous runs. Some time, they may use some common materials to clear or using cotton waste to clearing the residues or some special chemicals to clean it. It may consume material and/or men or there is some amount of cost associated with the operations.

On the other hand, if we have to place an order as in the case of a Stockist/Dealer, the cost may range from simple clerical plus stationers plus postage to complex estimates such as placing a quotation. Here again it consumes labor and/or material, and finally can be bringing down to a cost element associated with it.

Thus, this is the cost incurred with the placement of an order or with the initial preparation of production facility such as resetting the equipment for production. The set up cost is usually independent of the quantity ordered or size of the production run.

2. Production cost (or) Selling Price.(C)

It is the actual price; an item is produced or purchased (sold). In case of production it is the cost of producing an item and it may be a constant or variable one.

3. Holding cost (or) Storage cost (or) Carrying cost.(C1)

This represents the cost of carrying inventory in storage. It includes the interest on invested capital, storage space cost, insurance and handling cost. Holding costs are usually assumed to vary directly with the level of inventory as well as the length of the time the item is held in stock.

Holding cost consists of so many components with it and the type of storage such as own warehouses to rental warehouses, makes things much more complicated than expected. Above all, the accounting practices of many organizations may not support or sound enough to decide the cost estimates. Even though, the company owns the storage space, electricity expenses are met, the policies may not be very clear to arrive at the opportunity cost forgone by owning these facilities.

4. Shortage cost. (C2)

These are the penalty cost incurred as a result of running out of stock, when the commodity is needed. It generally includes the costs, due to loss of production, cost of idle equipment, the loss of goodwill of customers and the penalty of missing the delivery schedule.

In a study on FMCG segments, the stock out percentages of 85 prime brands, were estimated roughly around 25%, which means, out of these 85 fast moving brands, on an average, nearly 20 brands will be out of stock 4. These 85 brands, was in a position to control roughly 20% market share of the FMCG segment. The amount of revenue loss and loss of good will and ultimately loss of the customer base are going to be the consequences of shortages.

Recent survey reports of NCEAR say that brand switching is a common phenomenon in most of the FMCG product lines. Above all, the companies are trying for the same market share through the variety of consumer promotion tools. During the year 2001, almost 25-30 consumer promotions were offered in a month against the average of 5-6 5. In the case of rural consumers, the rate of brand switching is much higher than the urban chaps 6.

Some of the companies while purchasing make it compulsory to include a class on treatment on missing the scheduled delivery. Most of the times, very huge penalty such as the loss estimated as the case of missed scheduled will be entirely borne by the supplier and the missed scheduled used to estimate the performance of the vendor/seller/suppliers.

5. Demand. (D)

Demand is the number of units required per period and may be known exactly or known in terms of probabilities.

Problems in which demand is assumed to be a random variable are called stochastic problems. The demand is invariably probabilistic in nature for many real time situations. For some of the products, the demand may be seasonal also, such as soft drinks, cement etc.

6. Lead-time

When an order is placed it may be of instantaneous delivery or it may require some time before delivery is effected. The time between the placement of order and its receipt is called lead-time. Again the lead-time may also follow probability distribution. I.e., the lead-time is certain or uncertain. Consider the example of a FMCG Distribution channel, which faced lot of problems with high amount of inventory and distribution efficiency.

7. Stock Replenishment

Getting stocks again is called replenishment. Instantaneous replenishment occurs when the stock is purchased from outside. Uniform replenishment may occur when the procured from local manufacturer.

For example, an automobile manufacturer purchasing Tyres from the local Original Equipment Manufacturer, used to get stocks at some fixed intervals say everyday one truckload or 1000 Tyres instead of getting the entire estimated demand of 30,000 Tyres in a month at once. Some of the parts such as screws and bolts etc can be purchased at bulk and stored. Here the entire demand for the month is supplied at once.

8. Inventory control with known demand

Inventory control problem in which demand is assumed to be fixed and completely known is called Economic Order Quantity (EOQ) problems. If it is the context of production, the batch size to be produced is fixed and completely determined in advance, and then it is known as Economic Lot Size problems.

9. Buffer Stock or Safety Stock

Generally demand is uncertain and cannot be pre determined completely. Lead-time is not always known exactly. The revenue forgone by not keeping adequate inventory i.e., cost of under stocking and sometimes payment of penalty for not meeting the delivery schedule are consequences of inadequate inventory levels. To overcome the situations of uncertainty in demand and lead-time, some extra stock is advisable so that shortages may not occur. This extra stock is known as buffer stock.

Tags : Operations Management - Transportation / Assignment & Inventory Management

Last 30 days 688 views