Accounting For Managers - Accounting Process

Journal

When a business transaction takes place, the first record of it is done in a book called journal. The journal records all the transactions of a business in the order in which they occur.

The journal may therefore be defined as a chronological record of accounting transactions. It shows names of accounts that are to be debited or credited, the amounts of the debits and credits and any other additional but useful information about the transaction. A journal does not replace but precedes the ledger. A proforma of a journal is given in illustration

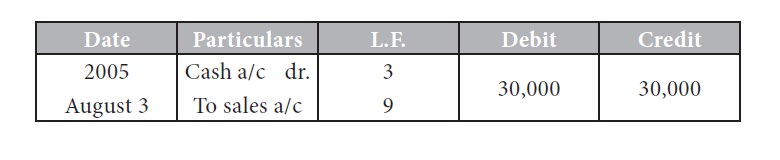

Illustration 1:

Journal

In illustration 1 the debit entry is listed first and the debit amount

appears in the left-hand amount column; the account to be credited appears

below the debit entry and the credit amount appears in the right hand amount

column. The data in the journal entry are transferred to the appropriate

accounts in the ledger by a process known as posting. Any entry in any account

can be made only on the basis of a journal entry. The column l.f. which stands

for ledger folio gives the page number of accounts in the ledger wherein

posting for the journal entry has been made. After all the journal entries are

posted in the respective ledger accounts, each ledger account is balanced by

subtracting the smaller total from the bigger total. The resultant figure may

be either debit or credit balance and vice-versa.

Thus the transactions are recorded first of all in the journal and then

they are posted to the ledger. Hence the journal is called the book of original

or prime entry and the ledger is the book of second entry. While the journal

records transactions in a chronological order, the ledger records transactions

in an analytical order.