Home | ARTS | Strategic Management

|

Decision-Making Hierarchy Of Business Firms - Strategic Business Unit and Functional Level Strategies

Strategic Management - Concept Of Corporate Strategy

Decision-Making Hierarchy Of Business Firms - Strategic Business Unit and Functional Level Strategies

Posted On :

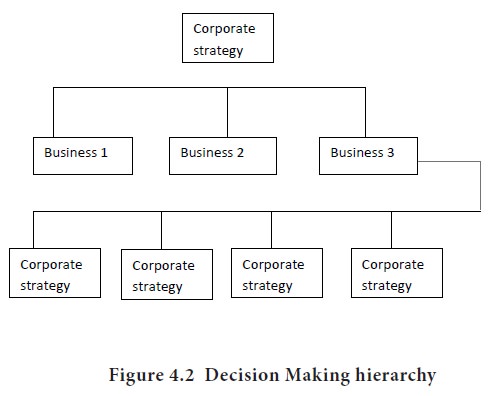

The decision-making hierarchy of business firms typically con-tains three levels as shown in Figure 4.2

Decision-Making Hierarchy

Of Business Firms

The decision-making hierarchy of business firms typically con-tains three levels as shown in Figure 4.2 At the top is the corporate level, composed principally of members of the board of directors and the chief executive and administrative officers. They are responsible for the fi-nancial performance of the corporation as a whole and for achieving the

The second rung of the decision-making hierarchy is

the business level composed principally of business and corporate mangers.

These managers must translate the general statements of directions and intent

generated at the corporate level into concrete, functional objectives and

strategies for individual business divisions or SBUs. In essence, business-level

strategic mangers must determine the basis on which a company can compete in

the selected product-market arena.

The third rung is the functional level, composed principally of managers of product, geographic, and functional areas . It is their responsibility to develop annual objectives and short-term strategies in such areas as production, operations, and research and development; finance and accounting, marketing: and human relations. However, their greatest responsibilities are in the implementation or execution of a company’s strategic plans. While corporate and business-level managers centre their planning concerns on “doing the right things,” managers at the functional level must stress “doing things right.” Thus, they directly address such issues as the efficiency and effectiveness of production and marketing systems, the quality and extent of customer service, and the

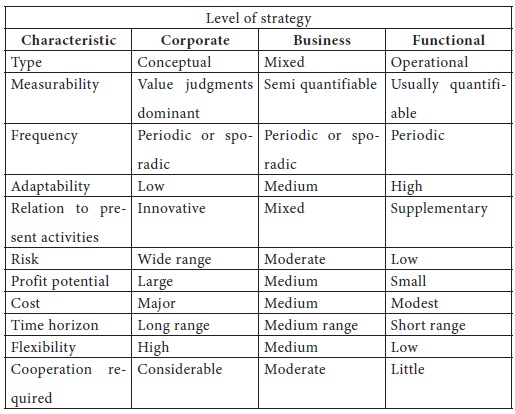

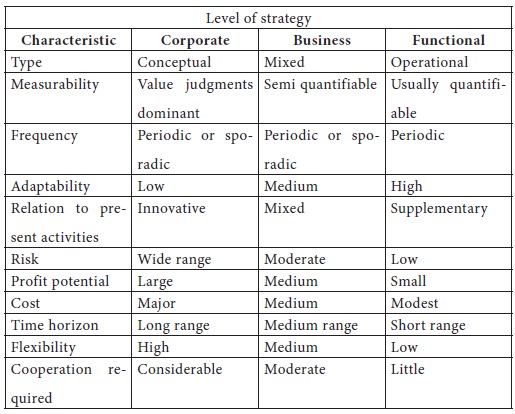

Table 4-1 depicts the characteristics of strategic

manage-ment decisions at different levels. Examples of corporate-level

decisions include the choice of business, dividend policies, sources of

long-term financing, and properties for growth. Functional-level decisions

usu-ally determine actions requiring minimal company wide cooperation. These

activities supplement the functional area’s present activities and a re

adaptable to ongoing activities so that minimal cooperation is needed for

successful implementation. Business –level descriptions of strategic decisions

fall between those for the other two levels. For example, busi-ness-level

decisions are less costly, risky, and potentially profitable than corporate

level decisions, but they are more costly, risky, and potentially profitable

than functional-level decisions. Some common business-level decisions involve

plant location marketing segmentation and geographic coverage, and distribution

channels.

Table 4-1

Characteristics of strategic management decisions at different levels

The decision-making hierarchy of business firms typically con-tains three levels as shown in Figure 4.2 At the top is the corporate level, composed principally of members of the board of directors and the chief executive and administrative officers. They are responsible for the fi-nancial performance of the corporation as a whole and for achieving the

The third rung is the functional level, composed principally of managers of product, geographic, and functional areas . It is their responsibility to develop annual objectives and short-term strategies in such areas as production, operations, and research and development; finance and accounting, marketing: and human relations. However, their greatest responsibilities are in the implementation or execution of a company’s strategic plans. While corporate and business-level managers centre their planning concerns on “doing the right things,” managers at the functional level must stress “doing things right.” Thus, they directly address such issues as the efficiency and effectiveness of production and marketing systems, the quality and extent of customer service, and the

Tags : Strategic Management - Concept Of Corporate Strategy

Last 30 days 1996 views