Accounting For Managers - Management Accounting-Cost Volume Profit Analysis

Summary and Case Analysis-Cost Volume Profit Analysis

Posted On :

Cost-volume-profit analysis is a technique of analysis to study the effects of cost and volume variations on profit.

Summary

Cost-volume-profit analysis is a technique of analysis to study the effects of cost and volume variations on profit. It determines the probable profit at any level of activity. It helps in profit planning, preparation of flexible budgets, fixation of selling prices for products, etc.

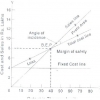

The break-even point is generally depicted through the break-even chart. The chart shows the profitability of an undertaking at various levels of activity. It brings out the relationship between cost, volume and profit clearly. On the negative side, the limitations of break-even analysis are: difficulty in segregating costs into fixed and variable components, difficulty in applying the technique to multi-product firms, short-term orientation of the concept etc.

Case Analysis

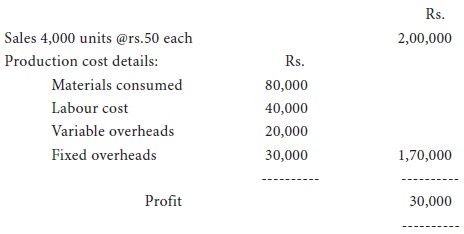

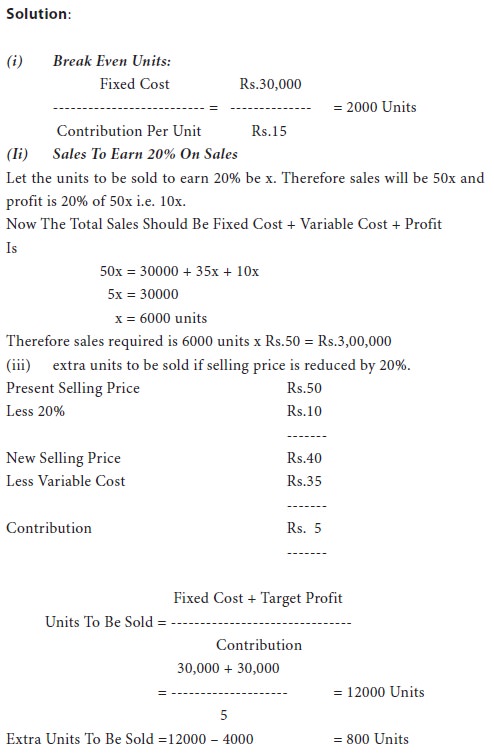

The directors of anandam ltd. Provide you the following data relating to the cylce chain manufactured by them:

They require you to answer their following queries:

(i) the number of units by selling which the company will be At break-even.

(ii) the sales

needed to earn a profit of 20% on sales.

(iii) the extra units which would be sold to obtain the present Profit if it is proposed to reduce the selling price by 20%

(iii) the extra units which would be sold to obtain the present Profit if it is proposed to reduce the selling price by 20%

Tags : Accounting For Managers - Management Accounting-Cost Volume Profit Analysis

Last 30 days 717 views