Financial Management - Finance – An Introduction

Finance in Relation to Other Allied Disciplines

Posted On :

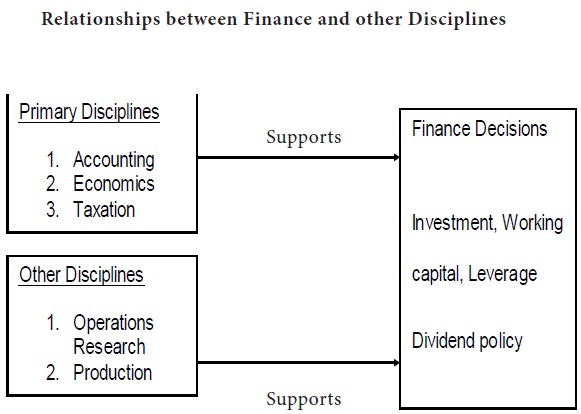

The finance function cannot work effectively unless it draws on the-disciplines which are closely associated with it.

Finance in Relation to Other Allied Disciplines

The finance function cannot work effectively unless it draws on the-disciplines which are closely associated with it. Management is heavily dependent on accounting for operating facts. Accounting’ has been described by Richard M. Lynch and Robert W. Williamson as “the measurement and communication of financial and economical data. In fact, accounting information relates to the production, sales, expenses, investments, losses and gains of the business. Accounting has three branches namely, financial accounting, cost accounting and management accounting.

It is concerned with the preparation of reports which provide information to users outside the firm. The most common reports are the financial statements included in the annual reports of stock-holders and potential investors. The main objective of these-reports is to inform stockholders, creditors and other investors how assets are controlled by a firm. In the light of the financial statements and certain other information, the accountant prepares funds film statement, cash flow statement and budgets.

A master plan (Budget) of the organization includes and coordinates the plans of every department in financial terms. According to Guthmann and Dougall, “Problems of finance are intimately connected while problems of purchasing, production and marketing”.

It deals primarily with cost data. It is the process of classifying, recording, allocating and reporting the various costs incurred in the operation of an enterprise. It includes a detailed system of control for material, labour and overheads. Budgetary control and standard casting are integral part of cost accounting. The purpose of cost accounting is to provide information to the management for decision making, planning and control. It facilitates cost reduction and cost control. It involves reporting of cost data to the management.

It refers to accounting for the management. It provides necessary information to assist the management in the creation of policy and in the day to day operations. It enables the management to discharge all its functions, namely, planning, organizing, staffing, direction and control efficiently with the help of accounting information. Functions of management accounting include all activities connected with collecting, processing, interpreting and presenting information to the management. According to J. Batty, ‘management accounting’ is the term used to describe the accounting methods, systems and technique which coupled with special knowledge and ability, assist management in its task of maximizing profits or minimizing losses. Management accounting is related to the establishment of cost centres, preparation of budgets, and preparation of cost control accounts and fixing of responsibility for different functions.

The finance function cannot work effectively unless it draws on the-disciplines which are closely associated with it. Management is heavily dependent on accounting for operating facts. Accounting’ has been described by Richard M. Lynch and Robert W. Williamson as “the measurement and communication of financial and economical data. In fact, accounting information relates to the production, sales, expenses, investments, losses and gains of the business. Accounting has three branches namely, financial accounting, cost accounting and management accounting.

Financial Accounting

It is concerned with the preparation of reports which provide information to users outside the firm. The most common reports are the financial statements included in the annual reports of stock-holders and potential investors. The main objective of these-reports is to inform stockholders, creditors and other investors how assets are controlled by a firm. In the light of the financial statements and certain other information, the accountant prepares funds film statement, cash flow statement and budgets.

A master plan (Budget) of the organization includes and coordinates the plans of every department in financial terms. According to Guthmann and Dougall, “Problems of finance are intimately connected while problems of purchasing, production and marketing”.

Cost Accounting

It deals primarily with cost data. It is the process of classifying, recording, allocating and reporting the various costs incurred in the operation of an enterprise. It includes a detailed system of control for material, labour and overheads. Budgetary control and standard casting are integral part of cost accounting. The purpose of cost accounting is to provide information to the management for decision making, planning and control. It facilitates cost reduction and cost control. It involves reporting of cost data to the management.

Management Accounting

It refers to accounting for the management. It provides necessary information to assist the management in the creation of policy and in the day to day operations. It enables the management to discharge all its functions, namely, planning, organizing, staffing, direction and control efficiently with the help of accounting information. Functions of management accounting include all activities connected with collecting, processing, interpreting and presenting information to the management. According to J. Batty, ‘management accounting’ is the term used to describe the accounting methods, systems and technique which coupled with special knowledge and ability, assist management in its task of maximizing profits or minimizing losses. Management accounting is related to the establishment of cost centres, preparation of budgets, and preparation of cost control accounts and fixing of responsibility for different functions.

Tags : Financial Management - Finance – An Introduction

Last 30 days 1281 views