Accounting For Managers - Basics of Accounting

Scope And Functions Of Accounting

Individuals engaged in such areas of business as finance, production, marketing, personnel and general management need not be expert accountants but their effectiveness is no doubt increased if they have a good understanding of accounting principles. Everyone engaged in business activity, from the bottom level employee to the chief executive and owner, comes into contact withaccounting. The higher the level of authority and responsibility, the greater is the need for an understanding of accounting concepts and terminology.

A study conducted in united states revealed that the most common

background of chief executive officers in united states corporations was

finance and accounting. Interviews with several corporate executives drew the

following comments:

“…… my

training in accounting and auditing practice has been extremely

valuable to me throughout”. “a knowledge of accounting carried with it

understanding of the establishment and maintenance of sound financial controls-

is an area which is absolutely essential to a chief executive officer”.

Though accounting is generally associated with business, it is not only

business people who make use of accounting but also many individuals in

non-business areas that make use of accounting data and need to understand

accounting principles and terminology. For e.g. An engineer responsible for

selecting the most desirable solution to a technical

manufacturing

problem may consider cost accounting data to be the decisive factor. Lawyers

want accounting data in tax cases and damages from breach of contract.

Governmental agencies rely on an accounting data in evaluating the efficiency

of government operations and for approving the feasibility of proposed taxation

and spending programs. Accounting thus plays an important role in modern

society and broadly speaking all citizens are affected by accounting in some

way or the other.

Accounting which is so important

to all, discharges the following vital functions:

Keeping Systematic Records:

This is

the fundamental function of accounting. The transactions of the business are

properly recorded, classified and summarized into final financial statements –

income statement and the balance sheet.

Protecting The Business Properties:

The

second function of accounting is to protect the properties of the business by

maintaining proper record of various assets and thus enabling the management to

exercise proper control over them.

Communicating

The Results:

As

accounting has been designated as the language of business, its third function

is to communicate financial information in respect of net profits, assets,

liabilities, etc., to the interested parties.

Meeting

Legal Requirements:

The

fourth and last function of accounting is to devise such a system as will meet

the legal requirements. The provisions of various laws such as the companies

act, income tax act, etc., require the submission of various statements like

income tax returns, annual accounts and so on. Accounting system aims at

fulfilling this requirement of law.

It may be noted that the

functions stated above are those of financial accounting alone. The other

branches of accounting, about which we are going to see later in this lesson,

have their special functions with the common objective of assisting the

management in its task of planning, control and coordination of business

activities. Of all the branches of accounting, management accounting is the

most important from the management point of view.

As accounting is the language of business, the primary aim of

accounting, like any other language, is to serve as a means of communication.

Most of the world’s work is done through organizations – groups of people who

work together to accomplish one or more objectives. In doing its work, an

organization uses resources – men, material, money and machine and various

services. To work effectively, the people in an organization need information

about these sources and the results achieved through using them. People outside

the organization need similar information to make judgments about the

organization. Accounting is the system that provides such information.

Any system has three features, viz., input, processes and output.

Accounting as a social science can be viewed as an information system, since it

has all the three features i.e., inputs (raw data), processes (men and

equipment) and outputs (reports and information). Accounting information is

composed principally of financial data about business transactions. The mere

records of transactions are of little use in making “informed judgments and

decisions”. The recorded data must be sorted and summarized before significant

analysis can be prepared. Some of the reports to the enterprise manager and to

others who need economic information may be made frequently; other reports are

issued only at longer intervals. The usefulness of reports is often enhanced by

various types of percentage and trend analyses. The “basic raw

materials” of accounting are composed of

business transactions data. Its “primary end products” are composed of various

summaries, analyses and reports.

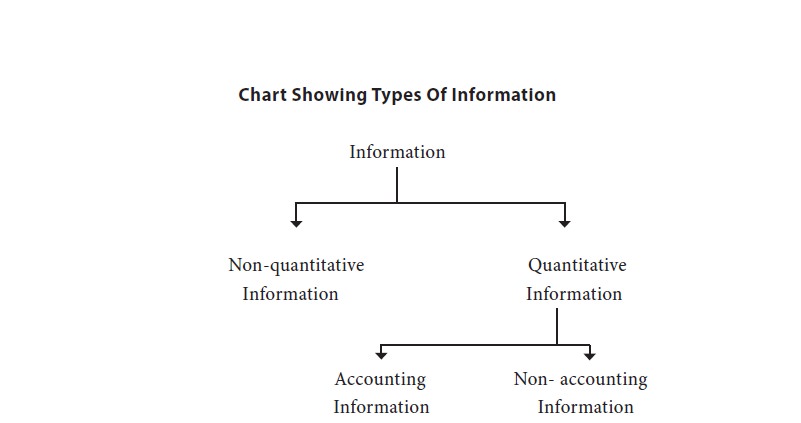

The information needs of a business enterprise can be outlined and

illustrated with the help of the following chart:

The chart

clearly presents the different types of information that might be useful to all

sorts of individuals interested in the business enterprise. As seen from the

chart, accounting supplies the quantitative information. The special feature of

accounting as a kind of a quantitative information and as distinguished from

other types of quantitative information is that it usually is expressed in

monetary terms.

In this

connection it is worthwhile to recall the definitions of accounting as given by

the american institute of certified and public accountants and by the american

accounting principles board.